Is The Pink Flamingo on the Brink of Collapse?

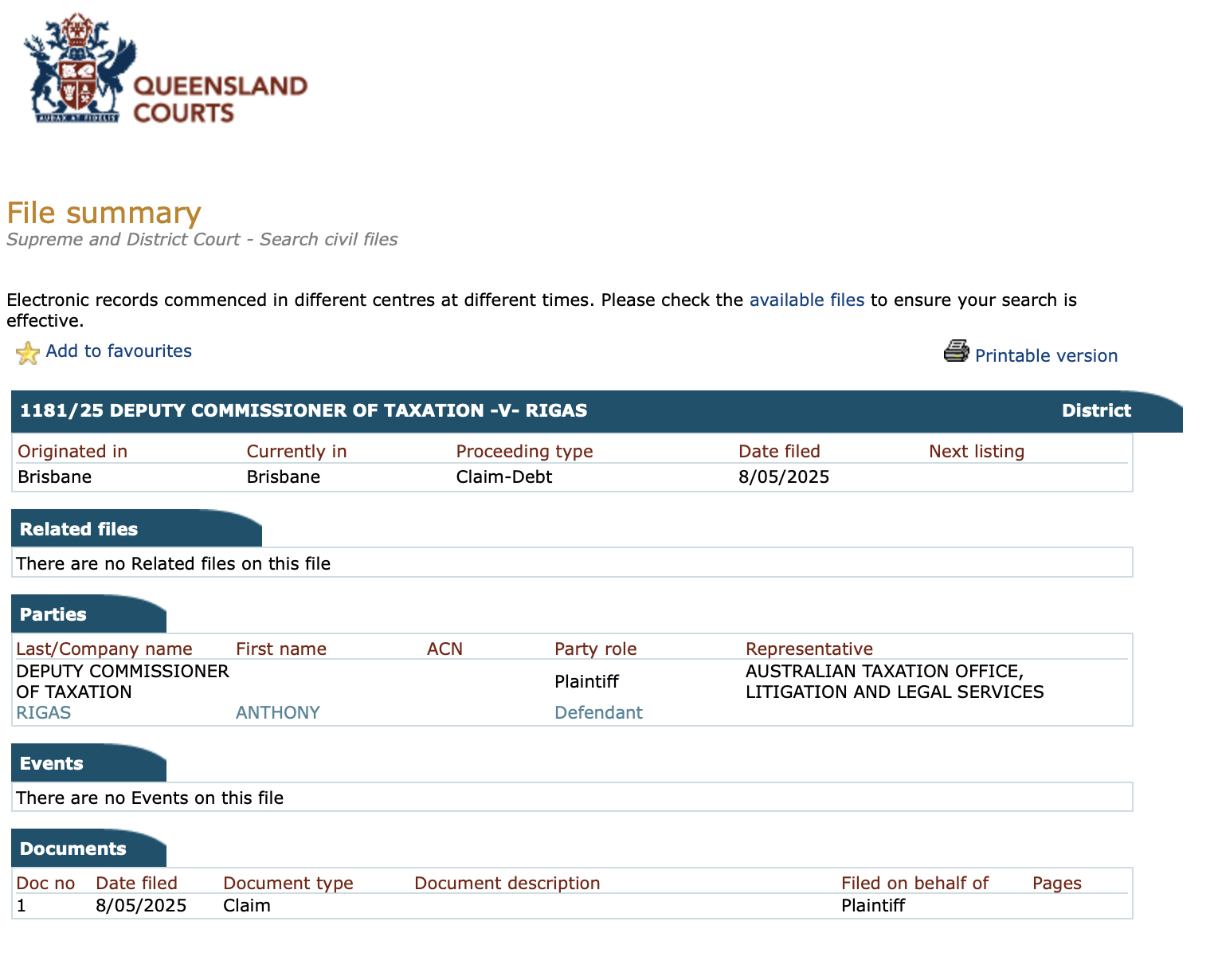

The Australian Taxation Office has initiated legal action against former cabaret owners Anthony ‘Tony’ Rigas and Susan Porrett, raising questions about the future of the Gold Coast cabaret venue.

Step into the Pink Flamingo Spiegelclub on the Gold Coast and the scene seduces at once. Sequined showgirls shimmer under hot pink light. Aerial artists glide through the air while coupe glasses catch the glow like tiny mirrors. The atmosphere insists upon glamour, a European cabaret conjured on Broadbeach, a place built to make skepticism feel gauche and hard questions feel out of place. The music swells, the applause comes on cue, and for many a patron the night ends with a grin.

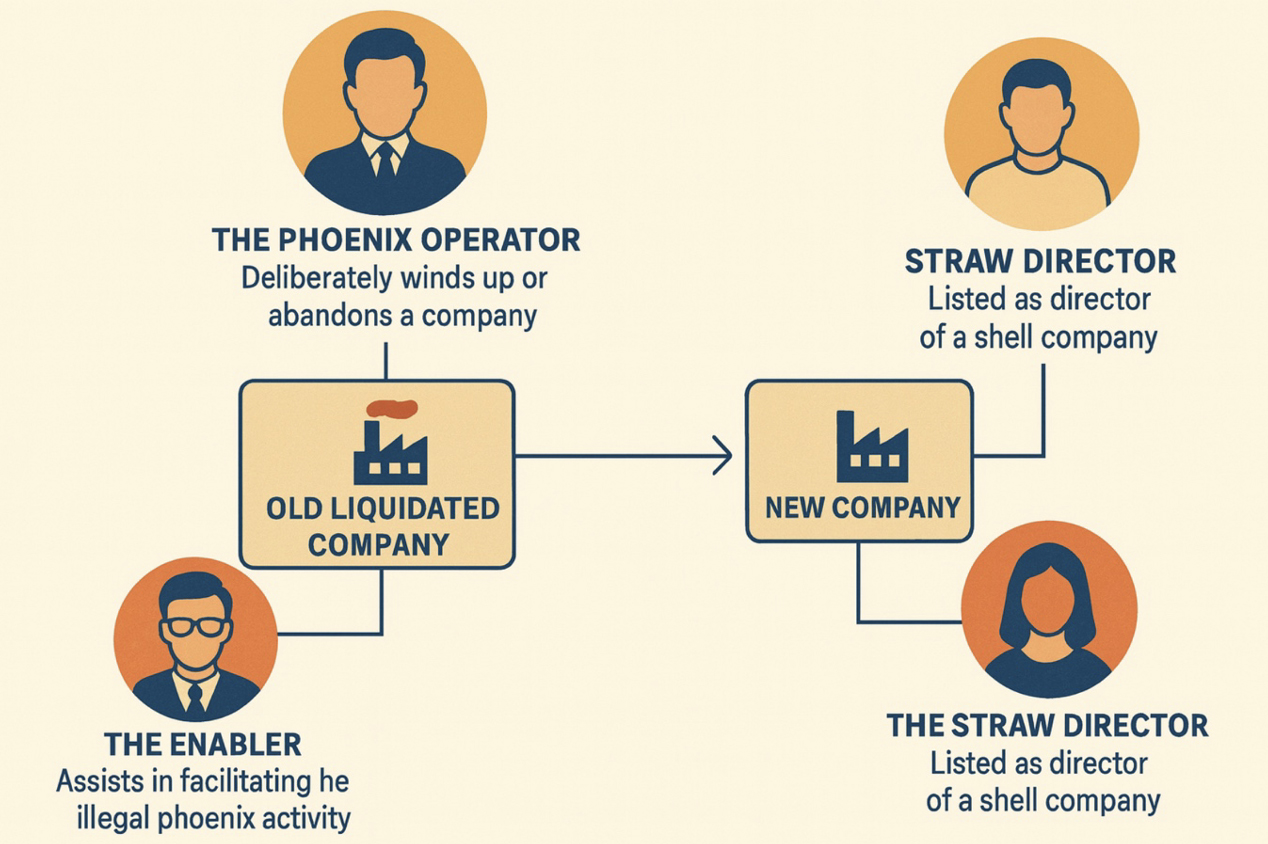

The curtain might as well fall there. It does not. Behind those feathers, behind the champagne and neon, lies a pattern that refuses to applaud or smile. It is a pattern of liquidations, sudden corporate handoffs, and debts that never seem to find their way home. Wages and superannuation go missing. Suppliers wait and wait. Then the nameplate on the door changes and the show goes on, as if the past has been airbrushed away. The story is not novel in the Australian entertainment economy. It is the familiar silhouette of phoenixing, a practice regulators describe plainly, when one company collapses under debt, then a near twin appears almost at once, carrying on the same business while leaving creditors behind.

This feature traces that silhouette in detail. It is suspicious in tone because caution is the only sensible way to tell it. It is investigative in approach because the questions it raises demand more than ambience. Can a nightlife brand keep reinventing itself on paper while leaving real people, real tax obligations, and real bills unpaid, and still call that reinvention success. How many times can a brand be reborn before the audience realizes the trick lies not in spectacle, but in corporate choreography that shuffles the risk away from insiders and onto everyone else.

What follows pulls together statements, transactions, timelines, and first-hand accounts to examine how the Pink Flamingo story came to look like a case study in the cycle regulators warn about. The quotes that appear in this feature are reproduced, exactly as they were recorded, because nothing should be softened or paraphrased when public trust and people’s money are in the balance.

Act One, The Ringleaders Behind the Curtain

The narrative thrust comes down to three principal operators, Susan Porrett, Tony Rigas, and his steadfast accomplice, Louise Huxham. Their public images differ, but the outcomes of the entities they touch tend to rhyme. Porrett presents as a champion of the arts and supporter of performing artists. The depiction reads like a press kit. The working reality, according to those who have traced the money, looks transactional, advocacy turned to leverage, friendships pressed into service of an enterprise that appears to reward the inner circle and leave obligations to others unsettled.

Tony Rigas wears a different mask. He rarely bothers with the language of altruism. His résumé is a list, a long one, a legacy of failed hospitality ventures that began loud and ended quiet. Shooters Saloon, Opium, Vodka and Champagne Bar, All Stars Sports Bar, The Monkey Cage, Delano Hotel, Love Nightlife, Club Boutique, The Oriental Whiskey Bar, East Nightclub, 2 Tribes, Little Shop of Big Ideas, Moonshine Bros. The pattern leaves onlookers wondering where misfortune ends and method begins. As one reader put it with bleak economy;

Going under with unpaid bills one time is sad, twice is unfortunate, 8 times is well….let’s just say it sounds more like a business plan than unfortunate accident.

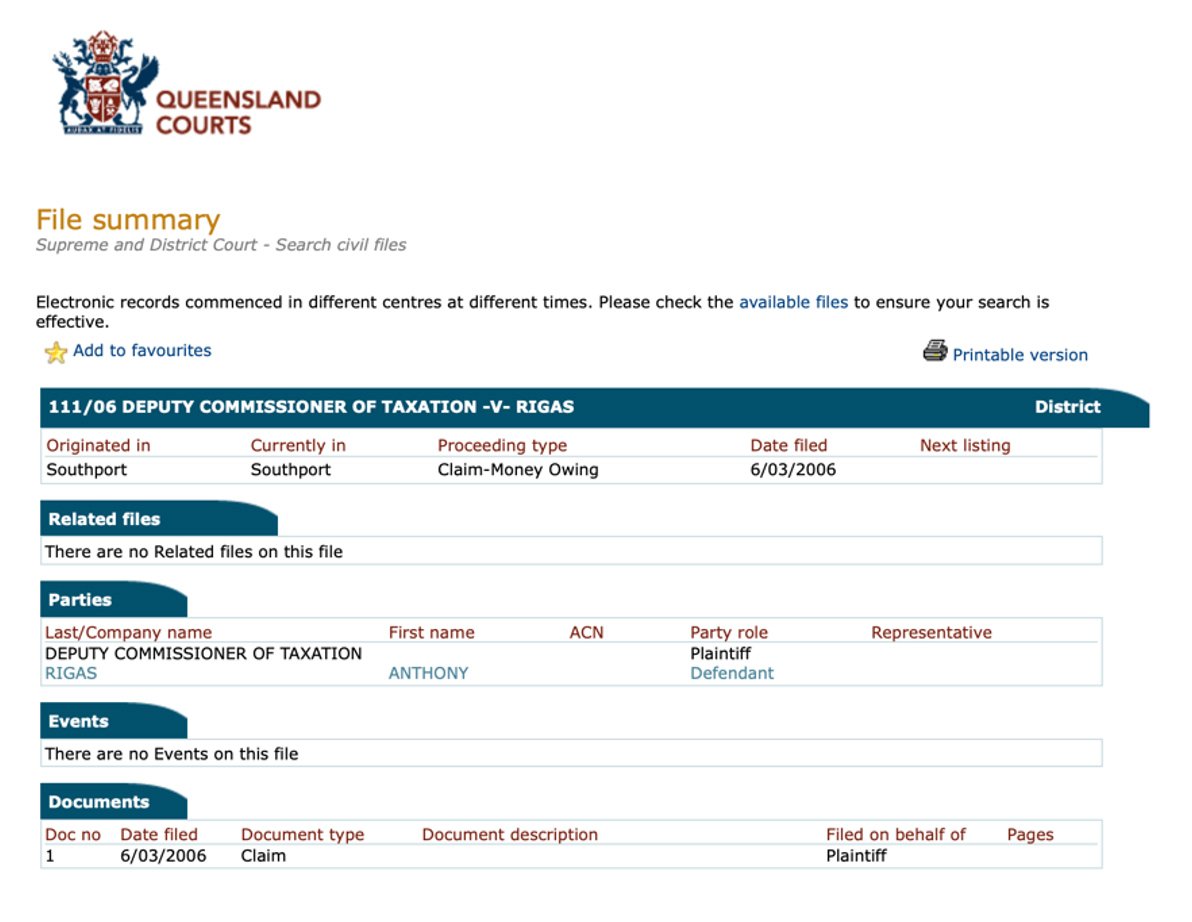

History is not just prologue here, it is context. Rigas’s engagements with the Australian Taxation Office stretch back nearly two decades, ending at one point in bankruptcy and an exit to Thailand, followed by more of the same.

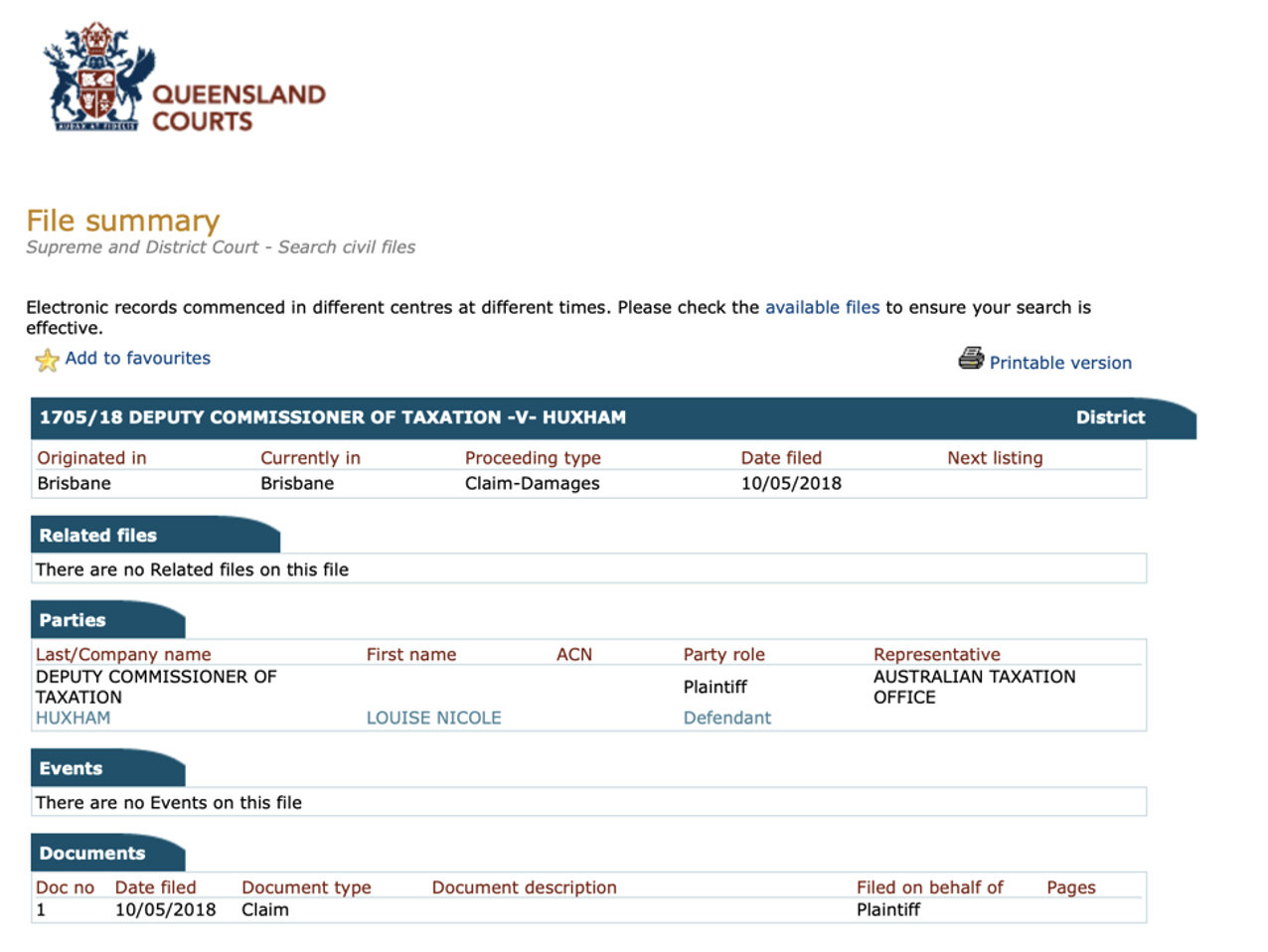

Huxham’s relationship with the tax office is not distant either, with action against her surfacing in 2018. In 2025, the tax office presence in this story is again pronounced. The analogy put to these two is pointed, forget Thelma and Louise, the suggestion goes, and think instead of a suburban Bonnie and Clyde of the balance sheet.

Intent matters. That is a legal concept and a moral one. In corporate disputes, especially where creditors are left unpaid, the divide between incompetence and design matters a great deal. In prosecution, intent is everything because it distinguishes between an accident and a crime. The law is not simply about what happened, but why it happened. Prosecutors must show that a person acted with a guilty mind, what lawyers call mens rea, to prove the act was not mere incompetence or misfortune but a deliberate attempt to deceive, defraud, or exploit. Without intent, defendants can hide behind claims of ignorance, error, or bad luck. With intent established, their conduct is exposed as a conscious scheme. This is especially crucial in financial crime, businesses fail all the time, but when a collapse is engineered, when directors knowingly strip assets, mislead creditors, or plan the fallout, it becomes criminal. Intent transforms negligence into fraud and makes the difference between a mistake and a calculated betrayal.

Place these three within that frame and a picture emerges. It does not depict a creative powerhouse. It depicts a triangle of aligned interests and outcomes. The triangle is stable because the costs fall outward. Investors, artists, staff, and the public purse absorb the damage. The show, however, appears to find a way to continue.

Act Two, The First Cracks, Ticket Money and Super

Industry sources raised an early alarm about a basic safeguard, the treatment of ticket revenue for shows that had not been delivered. Under the Live Performance Australia Ticketing Code of Practice, the principle is clear. Ticket money is to be held securely, in a trust account, until the show is performed. That approach protects consumers if a performance is cancelled or rescheduled. It also discourages operators from using tomorrow’s capital to pay yesterday’s bills. Without this safeguard in place, money you thought would pay for a night out, may actually end up the downpayment for a liquidator, but more on that later.

Audiences assume this kind of protection exists. Reputable venues are LPA members and accept the oversight that comes with it. My investigations revealed Pink Flamingo is not a member of LPA. The result is stark. There is no code obligation to secure ticket funds, and no member complaint channel if shows do not proceed. Patrons buy a promise. If the company fails, a safety net does not exist.

Employee entitlements provide another early signal. Former operator Project 88 TPF Pty Ltd, under the direction of Rigas and Porrett, accrued hundreds of thousands of dollars of unpaid superannuation. When the liquidation report from Worrells arrived, signed by liquidator Jason Bettles, the document outlined a sale of the venue days before Project 88 TPF Pty Ltd was placed into liquidation, not to an arm’s length purchaser, but to an entity incorporated by Rigas’ defecto partner Louise Huxham, under KSAJ Group Pty Ltd. The brand did not change. The shows did not change. The staff did not change. The venue did not change. The performance schedule did not change. The branding did not change. The corporate shell did.

Act Three, Ego, Equity, and a Tent in Brisbane

Why take those risks. The simplest explanation offered by those close to the matter is a blend of ego and survival, a belief that more cashflow could outrun the gravitational pull of existing debt. They add that his history of bankruptcy and ongoing disputes with the ATO sharpened the calculus, since the imminent collapse of the Pink Flamingo Gold Coast could have triggered ATO recovery action against personal assets, including the Mermaid Waters residence held by Rigas and Huxham. By 2023, the ledger was heavy, around three million dollars owed, with the ATO claiming almost two million of that total. On 23 September 2023, Rigas and Huxham sold their Mermaid Waters home for 2.685 million Australian dollars. The mortgage was cleared. The equity unlocked. Roughly eight hundred and fifty thousand dollars became liquid.

Those funds were not used to pay off existing liabilities, including outstanding employee superannuation. They moved forward into a new spectacle. Brisbane’s Northshore would host Pink Flamingo Spiegeland. The marketing called it expansion. Skeptics called it a gamble. One insider condensed the decision to a sentence that deserves to be read twice, “It was a desperate play dressed up as a bold new venture,” they said. The look of confidence returned to the stage. The balance sheet did not share the feeling.

Spiegeland raised a tent in December 2023 and promised a new chapter. The chapter opened fast and messy. Costs rose. Receipts looked lumpy. Confidence eroded rather than compounded. The Brisbane project began to look less like growth and more like a way to buy time against the weight bearing down from the failing Gold Coast venue. The ATO was not going away. The debt did not evaporate. And in that context, capital kept moving around the inner circle.

One episode stands out for its brazenness. An insider account described Susan Porrett walking into the former Gold Coast head office with a shoebox stuffed with one hundred and fifty thousand dollars in banknotes, crediting the source to her “father’s old circus days.” The explanation did not endure scrutiny. The Australian Federal Police confirmed the $50 notes appear to be the newest issue of Australian polymer money, introduced on 18 October 2018 with anti fraud features. The image that remains is not nostalgia, but fresh cash fed into a business where unpaid super, unpaid suppliers, and unpaid tax were already part of the culture. The implication is obvious. Cash moved in small stacks while public debts went begging.

The story did not end with a shoebox. Financial evidence linked to Project 303 TPF Pty Ltd, the Brisbane vehicle, revealed withdrawals that were neither authorised nor accounted for, on numerous occasions. On the evening of 29 August 2024, thousands of dollars, of unauthorised funds, left the Project 303 bank account, to cover the deficit of payroll of the struggling Gold Coast venue. Later, Porrett suggested she thought it was acceptable. Pressed further, she admitted the funds had been taken and used to cover the weekly wages, with details vague. An investor discovered the transaction and lost temper and patience at once. He demanded that Porrett “put the money back you f**king thief.” The call ended. The reality did not. The incident read like a case study in control failures and personal use of company cash.

Porrett’s réponse “With this said, [Investor] is no longer to be involved in any part of The Pink Flamingo, including private financial conversations between directors.”

Email records show Porrett was met with the following critique:

It was bought to my attention that during the liquidation of Project 88 TPF Pty Ltd, Tony and Louise charged alcohol supplies for your new entity, KSAJ Group Pty Ltd, to the business account of Project 303 Pty Ltd, with no intention of settling the final bill. This action reflects a consistent pattern of behaviour that raises serious concerns. You, Sue, had previously assured me that these funds would be repaid, yet merely two days later, you dismissed this commitment, stating that the funds were unavailable. Given the known precarious financial state of Project 303, it is deeply troubling that you would divert funds from Project 303 to cover the payroll of KSAJ Group, a company that, by your own admission, was established to undermine its largest creditor, the ATO. This conduct is not only unethical but could potentially expose all parties involved to significant legal liability.

Within a year of the Gold Coast collapse, another pair of lenders entered the frame. Lumi Finance Pty Ltd and Shift Finance Pty Ltd supplied funds to Project 88 TPF Pty Ltd based upon documents that painted an optimistic picture. The optimism did not reach creditors later. It did reach the capital stack for Brisbane, where borrowed money appears to have been used in part to present as personal investment by insiders. The trail of receipts is thin. The optics are not.

Act Four, Shifty Loans, The Performance of a Narrative

As the Gold Coast entity teetered, the narrative shifted. In communication with investors, Rigas introduced a plotline about a one hundred thousand dollar loan from a gangster that had to be repaid or else. This detail unfolded at a shareholder meeting. The tone was confessional, the message, that events had forced him into a desperate deal to protect the larger project.

He did not downplay the cost, “It’s a $100,000 loan at 52% interest, a thousand a week….” he said. “I didn’t want to take that loan”. When challenged on the specifics, including the identity of the lender and the mechanics of repayment, the story tried to deepen itself through mood. “We went to loan sharks,” he said. “You start swimming with sharks… it’s never good. And that’s why I didn’t want to do it. I didn’t want to make that phone call. I was really uncomfortable with this, but our choices were limited.” The identity of the lender remained unspoken, “It’s a colourful character, and I’d rather not say his name, but it’s someone that if I said his name, we’d all know who it is. He’s owned plenty of clubs, bars, and restaurants in Melbourne.”

Behind those theatrical beats, bank records show a plainer reality. Regular transfers of several thousand dollars left the company account each month and landed in Rigas’s personal account, framed internally as interest on a loan that lacked paper. No board approval. No lender contract. No collateral terms. Just line items that drained cash while investors were assured that everything was under control.

Forensic accounting often looks dull to outsiders. In this case, the month by month list reads like a metronome, thousands of dollars were withdrawn to Rigas’ personal bank account. It is a pattern that speaks on its own. It is also a pattern that will not be explained by mood or metaphor.

Act Five, Lumi, Shift, and the Chessboard of Guarantees

The funds advanced by Lumi and Shift Finance came to more than eight hundred thousand dollars in combination. But who would lend to an insolvent company? Through a combination of creative accounting documents and personal guarantees, these lenders found comfort in approving these loans. The loans were not to Rigas or Porrett personally. They were to the company, Project 88 TPF Pty Ltd, that both Rigas and Porrett directed. Both individuals supplied personal guarantees. That distinction mattered greatly when the music stopped. Rigas had positioned himself with few attachable assets. A house had been sold. A luxury Range Rover was leased. Bankruptcy is a door he had used before and remained available if needed. Porrett took a different approach. She retained property, including a Burleigh Heads residence and a Varsity Lakes commercial property where she operates her doggy daycare business. The contrast is not small. It speaks to how personal risk was distributed. Following the liquidation of Project 88, Lumi Finance sought to recover funds from the guarantors. Upon demand for payment, by the lender, one guarantor questioned the validity of the lending agreement, based on the undisclosed insolvency of Project 88, at the time the loans were disbursed. After a brief investigation by AFCA (The Australian Financial Complaints Authority) that guarantor was released from any liability.

There is more. Portions of the Lumi and Shift funds appear in the Brisbane story as if they were Rigas and Porrett’s own capital contribution, pushed through Project 88 and presented as funding for fit out. The receipts are sparse. The descriptions do not square with a careful trail. Investors have reason to ask whether borrowed money became the cosmetic layer that made insider investment look larger and more committed than it was.

Act Six, The Phoenix Mechanics

The handover was not accidental. Audio recordings captured the language of intent. Rigas put it as process, “It is liquidating, moving all the assets and leases and everything into a new company and then sinking the other company after that is done.” The bluntness leaves little room for alternate readings. Porrett, in a call on 13 July 2024, made the plan even clearer;

“We are going to do a phoenix.”

The choreography involved the landlord, Anna Touma. Fixtures and fittings would be “taken” as rent arrears, which would have the effect of shifting control of those assets beyond a liquidator’s immediate reach. The landlord would then lease the venue in place to KSAJ Group Pty Ltd, the Huxham vehicle. The guarantor of that lease, none other than Susan Porrett herself.

The optics are unmistakable. Debt and wreckage remained with Project 88. The continuity of operation, the same brand, the same physical plant, and the same humans behind them, stood up under a new shell.

The debt puzzle tightened further. Lumi and Shift loans, taken by Project 88, were not parked within the new Gold Coast company. They were pushed toward Brisbane, a separate business, Project 303, that was then made to carry obligations it had not contracted. Porrett’s own words draw the line directly. “Tony’s not paying them through 88, 303 is not paying them. I had to guarantee them. I know I’ve put the money down, I know part of it’s 88.”

When pressed to identify who carried the debt, she said, “It is not taken by us [Rigas & Porrett] personally. It was taken by 88… It is now because there’s no 88. Do you know what I’m saying? It is us personally because we haven’t been able to send, to organize and confirm that payment that comes from 303… We’ve paid about three payments, three months, I believe.” Later, the frustration sharpened into a future tense lament, “At the end of the day, I’m the one that misses out here because he’s got a closed shop and can go and fly off to Greece. And this is all of our debt or whatever that whatever we’re using for 303 is all of our debt. So we just have to assign that, work that out.”

The meaning of those phrases is plain. There is an attempt to move liabilities around the chessboard so that the new Gold Coast entity can stand unburdened, while Brisbane, a different operation, absorbs what it did not incur. For regulators, that looks like something more elaborate than ordinary phoenixing. For investors, it looks like misdirection layered over debt dumping.

Act Seven, The Accountant’s Spin and the Shape of a Balance Sheet

Registered accountants in Australia operate under APES 110, a code of ethics that lifts independence and integrity out of theory and into daily practice. Their job is not to make stories look nicer. It is to make numbers true and to align corporate reporting with the reality of assets and liabilities so that creditors, investors, and the public are not misled.

A leaked call with the longtime accountant to Rigas, David Sidhu, reveals a posture that raises more questions than it answers. When challenged about charges that appeared to shuttle between Project 88 and Project 303 in ways that did not make sense, Sidhu blurred the company line into a personal one. “So we don’t call it Project 88. We call it Tony and Sue,” he said. That sentence is not a clerical flourish. It functions like a solvent that dissolves the boundaries that keep liabilities where they belong and keep personal obligations from being repainted as company ones, or vice versa.

When asked directly whether the manoeuvring amounted to fraud, Sidhu did not reject the label. He sidestepped the concept itself, “What is fraud?” he asked. It is not the kind of philosophical question one expects when employees are waiting for entitlements and the tax office is still out of pocket.

The tone of the call pushed urgency over evidence. “I’m saying 12 hours. I’m saying 12 more business hours. We’re done,” he said, invoking pressure from the ATO to prompt decisions without full documentation. He questioned the utility of substantiation, “Trying to prove that Tony and Sue paid for it. I don’t understand what that’s going to achieve.” The metaphor that followed was theatrical and grim;

It’s like having an open house and leaving all the shit on the table. Is that what we want to do? Leave cocaine there, leave guns and bullets. Everything there. So when someone walks in here. Oh, okay. Right. I’ll take a photo of that, that and that, and we’ll just send this off to the police. And the police can come in and take.

Accountants are supposed to calm situations like this with clarity and paper, not accelerate them with brinkmanship. The call did not dispel suspicion. It reinforced it.

Act Eight, The Liquidator’s Lane and the Cost of Scrutiny

Liquidation is supposed to be the process that restores order when companies cannot pay what they owe. The liquidator maps the assets, identifies voidable transactions, and, where appropriate, claws back value for creditors. In this case, creditors were told the liquidator’s budget was limited. In his first report, Worrells’ Jason Bettles noted the funds available to examine asset transfers from Project 88 TPF Pty LTD to KSAJ Group Pty Ltd were thin, and that deeper investigation would require creditor funding.

Behind closed doors, that limitation did not come as a surprise to the inner circle. “No, no, it’s a set fee — $10,500 [for the liquidator] … They do the basics. Unless there’s a creditor that wants more forensic accountancy done or anything like that, then they say, ‘Show us the money.’” Rigas explained. He then articulated exactly why the group wanted the intercompany accounts to look empty, “We don’t want anything saying Project 88 or 303 owes Project 88 money because then the liquidator is obliged to chase that money. Yes, and that would be bad.”

Reassurance followed, “The liquidator’s a voluntary liquidator … he’s got $10,500. He’s not going to be watching blueprints and investigating unless someone wants him to.” Porrett described the earliest phase as a tactic, “It just depends at the end of this 30 days if there are creditors that pipe up … it’s a bit of a holding pattern right now.” Rigas approved the performance, “So far so good. The liquidator from Worrells has been great … David our accountant’s been really, really helpful.”

There is history here too. ASIC once accused Bettles of conduct that facilitated phoenix activity in an unrelated matter, the Members Alliance collapse. The case was dismissed. Costs were awarded against ASIC. That does not convert accusation into fact. It does remind observers that a light touch approach at the edge of phoenix territory attracts scrutiny.

Act Nine, The Human Ledger

Numbers are impersonal. Their consequences are not. Former staff of Pink Flamingo describe months without superannuation paid. They describe being told, by late in the week, to hand out tickets for free just to fill a room that was not selling enough. “By Thursday or Friday, we’d be told to give them all away, anything to fill the room,” one ex employee said.

For audiences, the risk is subtler. Without LPA membership, there is no Code requirement to hold ticket revenue in trust until the show plays. If a company collects payment for future dates while standing near the edge of liquidation, the consumer exposure becomes acute. When the lights go out, refunds can go with them.

In Brisbane, the timing of transactions tells a story. In the weeks before Project 303 went under, Rigas and Porret continued to sell tickets for future shows, collecting money that could never buy the performance promised. “Very pissed off, I only paid for my hens night this morning,” one buyer wrote. Another said, “We better be getting refunded … can’t tell me they had no idea about this over the weekend when I spoke to the team and got the invoice.” Bank records, meanwhile, show transfers out to related entities and insiders, including reimbursements of personal expenses that have no place at the front of the queue when a company is insolvent.

Preferential payments in the approach to insolvency are not a mere faux pas. The Corporations Act 2001 speaks directly to directors who continue to incur debts when there are reasonable grounds to suspect insolvency. Section 588G addresses the duty to prevent insolvent trading. Section 588FE sets out voidable transactions, including unfair preferences. Sell tickets you cannot honor and pass the proceeds to a new related company, and you will invite both legal and moral condemnation.

Act Ten, Physical Assets, A Two City Game

In late February, the Brisbane venue became a waypoint for property in motion. On Monday the 23rd and Tuesday the 24th, witnesses describe Susan Porrett loading furniture, staging equipment, lighting and décor that had been purchased with investor funds. Days later, those same items appeared at the Gold Coast venue, now operated by KSAJ Group under Huxham. The color palette could not hide the lineage. Distinctive pink velvet and branded props do not travel incognito.

The timing tells its own story. In the days before liquidation, assets should be preserved for creditors, not shuffled to related parties. Moving them for someone else’s benefit undermines that basic duty, and if done deliberately, edges toward illegality. Creditors who trusted Worrells to handle the Brisbane Pink Flamingo with integrity were disappointed to learn that rightful assets were transferred for the Gold Coast, free of charge. This did not look like happenstance. It looked like design. Critics note that this was exactly why Jason Bettles from Worrell’s was handpicked by Rigas and Porrett for the Gold Coast and Brisbane appointments.

So. Yeah. Nice and tight. Okay. And I shouldn’t laugh, you know. You know. So so so so so. Yeah. So far so good. You know…..The liquidator so far Worrell’s have been great. – Tony Rigas

When questioned about the transfer of a range of assets and alleged phoenix activity linked to Rigas and Porrett, liquidator Jason Bettles said;

Further investigations you have queried us about can be undertaken but require funding the liquidation does not have, and I am not prepared to conduct such investigation on a speculative basis.

The imagery tells the story plainly: Porrett, once again at the centre of a collapsing company, salvaging assets for a “new” venture run by the same team that left Brisbane’s creditors behind. For those owed money by Project 303, the sight of Brisbane’s theatre fittings lighting up Gold Coast stages is more than insulting, it’s evidence of a deliberate pattern of deceit. Porrett’s vehicle appears central to the asset removal captured days before Brisbane entity Project 303 entered formal liquidation. Porrett says she was collecting costumes owned by her company, Aerial Angels, and denies involvement in the other two vans, which she says were removing assets under the direction of Rigas.

For the second time in less than a year, the Pink Flamingo brand has been gutted from within, its remains repurposed for profit while investors and employees are left in the ashes.

Act Eleven, The Broader Pattern, Phoenixing as Open Secret

None of this unfolds in a vacuum. Phoenixing is a known drain on the Australian economy. Billions are lost when directors collapse one company, shift the good parts to a new one, and leave the liabilities behind. Employees forgo entitlements. The tax office gets in line with everyone else. Suppliers lose goods and hope. The practice is brazen, in part, because the enforcement resources to police it are thin. The ATO’s Phoenix Taskforce exists. ASIC carries a mandate. But the legal tightropes are delicate and casework is expensive. Penalties are often too soft to deter repeat offenders.

Into that space steps a familiar type, an operator with patience for paperwork and impatience with paying debts, a person or trio for whom corporate shells are levers and money is a liquid that always finds a related channel. The Pink Flamingo story reads like a compressed version of that national problem. It has the choreography, the timing, the insiders, the sudden transfers, the new companies, and the old obligations that never make the crossing.

Act Twelve, The Current Scene, Warning Signs and Refrains

The latest chapter carries the contours of earlier ones. Heavily discounted tickets to pad attendance. Delayed payments to suppliers. Optimistic updates to stakeholders that strain belief when compared with accounts payable. Legal jargon or theatrical anecdotes deployed when questions become specific. The claim of a gangster loan will not be the last story. When debt and doubt recur, narrative becomes a tool.

The warnings for the public are not subtle. If a brand is not a member of the LPA scheme, your ticket purchase does not sit in trust to protect you. If a brand has a record of moving operations to new companies just ahead of insolvency, then the promise attached to a future date is not the same as a promise backed by a balance sheet. Buyers do not like to be told to beware. They should be told anyway. The safest habit, when patterns like these persist, is to purchase on the night, not months in advance, or at minimum to pay by a method that gives you recovery leverage should the show disappear.

Act Thirteen, What Accountability Would Look Like

Accountability here is not only about punishment. It is about repair and deterrence. It would look like thorough liquidations with sufficient budget and mandate to examine transfers of value in the months preceding collapse. It would look like independent accountants who insist on documentation rather than theatre when insider loans are claimed. It would look like lenders that tie covenants not only to interest coverage, but to representations about related party transfers, membership in consumer protection codes, and escrow practices for ticket revenue. It would look like directors who accept that personal solvency is not a cloak if they diverted money or property while creditors stood unsecured.

When operations are phoenixing in effect, even if not in explicit form, regulators should consider quick freezing of suspect transfers, faster public bulletins warning ticket buyers of insolvency risk, and coordination with landlords to prevent the quiet handover of fixtures and fittings as rent arrears when those assets should otherwise be available for a liquidator to marshal.

Show business understands narrative. That is not a criticism. It is the art. But when the same devices are used to keep employees patient, to keep investors at bay, and to lull customers into advance purchases while insolvency is a known risk, then narrative is no longer a creative tool. It becomes a shield. The promise that new capital is around the corner. The hint that a celebrity investor is interested. The story of an extraordinary loan from a “colourful character.” These keep the lights on for another month. They do not pay the super that remains overdue. They do not square the account with the ATO.

The gangster loan vignette is a case study. It asks listeners to substitute drama for diligence. It suggests that unusual measures were taken in a noble effort to save the enterprise. It works on emotion and time pressure. It works less well on auditors, courts, and regulators. Those audiences ask to see paper.

Curtain Call, But Not For Everyone

The Pink Flamingo can still mount a show. Audiences will still shout and clap. That is what cabaret does. But the balance sheets tell a different story, one of greed and misdirection, of obligations displaced and debts recycled. Rigas, Porrett, and Huxham have not invented phoenixing. They have executed their chapter with a mix of showmanship and administrative nerve that keeps the music playing while the costs pool elsewhere.

The final warning goes to the public because the public is the last investor asked to buy in. The Live Performance Australia Ticketing Code exists to prevent advance revenue from being spent before a show is delivered. Membership signals a willingness to be bound by that rule. Absence from the Code is a red flag in its own right. The Pink Flamingo operators have not embraced that safeguard. They continued to sell tickets, collect deposits, and move money between companies even as collapses kept finding new shells and new stages.

If you plan to buy, do it with eyes open. Consider paying close to the performance date. Use payment methods that preserve dispute rights. Ask whether the venue participates in LPA’s Code. Ask how refunds are handled if a show does not proceed. Ask whether ticket funds are held in trust. These questions are not rude. They are responsible. Because in this story, history does not simply repeat, it encores. When the music stops, it is often the audience, the workers, and the creditors who are left with the bill, while the company name over the door changes again and the pink lights flicker back on.

And if you work inside an operation that looks and sounds like this one, take notes. Keep your own records of hours and entitlements. Photograph equipment and serial numbers if you are responsible for them. Save emails. When the trucks pull up at night, and the props and lighting are loaded for a quick drive down the highway, it is not melodrama to wonder about the next morning. It is prudence.

A show is a promise. A ticket is a promise. A wage is a promise. Superannuation is a promise. A tax remittance is a promise. The stage can stand on promises again, but only if the people behind it stop treating the company as a costume that can be changed whenever the plot gets tight.

Epilogue, What The Audience Can Do

Pink lights can be beautiful, and they can distract. Journalism asks readers to look past the glow after the applause, and follow the money from the bar till to the bank. If that trail ends at a liquidation, and the same operators open the doors the next day under a new company, the show on offer is not only cabaret. It is corporate theatre.

There is a point when an audience, asked too often to suspend disbelief for another opening night, stops clapping. That is when phoenix activity fails, when the brand no longer convinces, when lenders hold back funds, and when liquidators are resourced to trace every box that left the building in the small hours. Until then, buyer beware is not a slogan. It is the only honest headline.

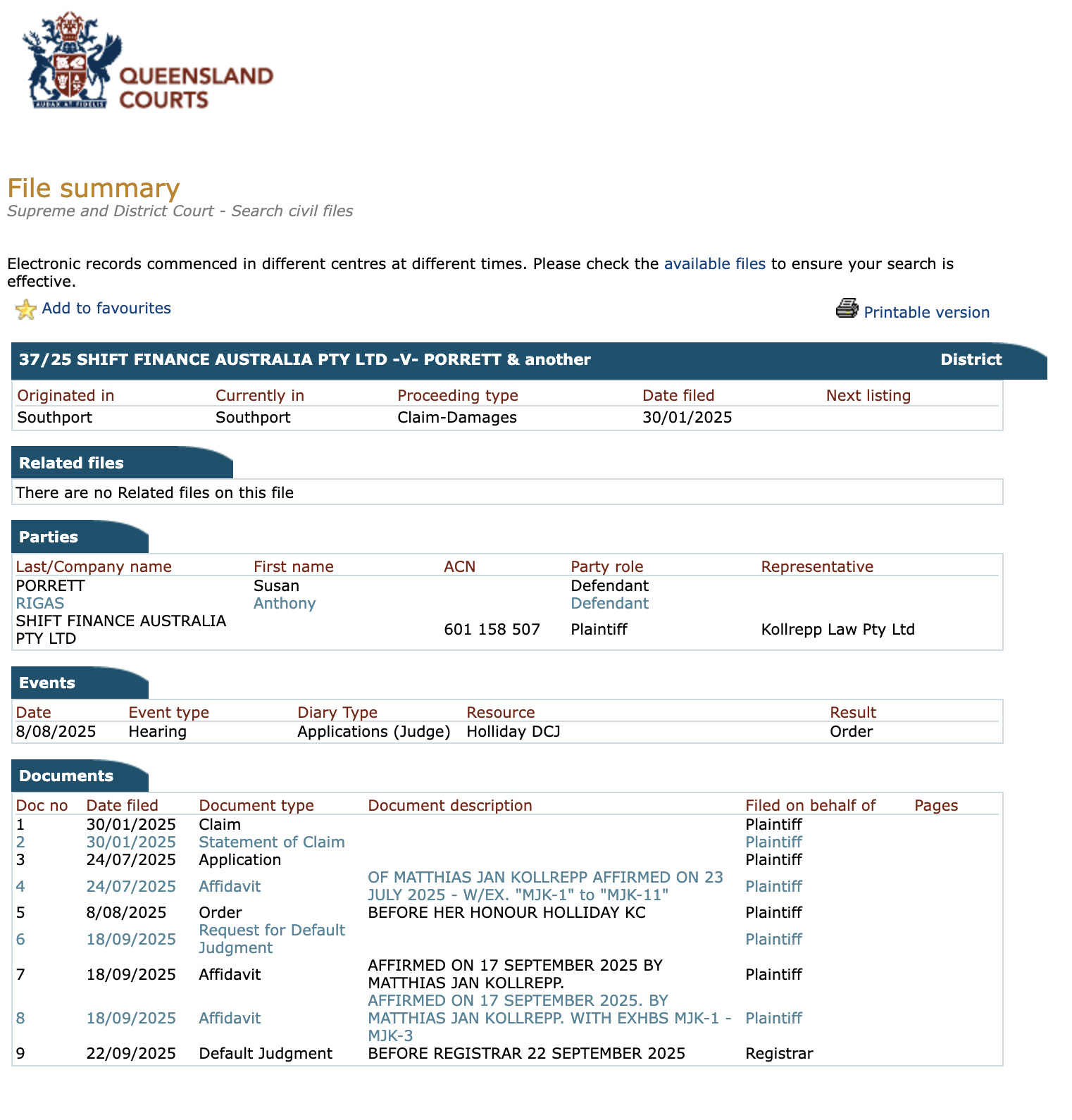

At the time of writing public court records show that the Australian Taxation Office are now actively pursuing both Susan Porrett and Anthony Rigas personally, so before the final curtain, perhaps these operators will be held accountable, with interest added.

Didn’t realise Rigas was into blokes, Huxham definitley has a dick

How have these three not been knocked off yet….

Rigas can hardly walk up a flight of stairs, his days are numbered. The evil gouls that took Willy Lopez in the movie Ghost will be waiting for the three of them when they are indoctrinated into the gates of hell.

I am so happy to see Porrett finally get what she deserves, serves her right for attacking me in Vegas.

Good grief, what insidious humans, absolutely appalling business ethics.

I personally know Louise Huxham, and herself and Tony are well known, amongst many locals to be not of the gentry. History has shown that this conduct never ends well.

This is an utter disgrace, Louise Huxham, Tony Rigas and Susan Porrett should be locked up. I am fed up paying tax for these cunts to rip off the system. Kudos to Sarah for exposing these criminals

Look out for Sue Porrett’s associates.. like all narcissistic abuses she has her flying monkeys! Aerial angels, dynamite studios, aerial angels school cirque central, Kate Grammatico, Dallas Dubois, Jordan Smith of duo resplendence, Jane mcphee. Protect your student and young performers from these people and their influence.

Look out for Sue Porrett’s associates continuing to work this way.. Aerial angels, dynamite studios, aerial angels school cirque central, Kate Grammatico, Dallas Dubois, Jordan Smith of duo resplendence, Jane mcphee, chase creations, Lee academy. Protect your students and young performers from these people and their influence.

Porrett, Rigas and Huxham should be locked up, they epitomise Gold Coast scum

as someone who’s been on the receiving end of sue and co’s financial abuse boy does this makes my little heart sing, I bet the rest of Sue’s counterparts from over the years are shaking in their boots right now….they know exactly who they are